History isn’t fact. It’s narrative.

When a startup business grows rapidly and is sold for hundreds of millions of dollars it’s easy to focus on the end point, and forget about the route. When the stories are retold over and over, details get rewritten or forgotten. And the bits that are omitted and updated are nearly always the stumbles or backward steps.1 As a result, others starting out on their own ventures and hoping for the same outcome rarely hear about these hard moments, and so they’re surprised when they happen to them too. It’s a mistake to assume that they won’t.

I’ve worked on and invested in some of New Zealand’s most successful startups. They have become household names. But I got to know each of them at the very beginning, when their success was far from obvious. I was an early employee at Trade Me and Xero and, thankfully in both cases, also a shareholder. The financial success of those companies afforded me a rare privilege: I could have chosen to never work again. Instead, I pursued a second act in my career as an early-stage investor and advisor at such startups as Vend, Timely and many others.

There are entertaining tales to tell about all of these companies, and a handful of days that were wonderful – in a couple of cases life-changing. But the truth is that they’re the fleeting exceptions. The real experience of building these ventures is much more about the long, hard grind well away from an audience than it is the magic moments in the spotlight. The norm is more a succession of frustrating (and expensive) small failures than glorious victories. Frankly told, the unvarnished inside stories would be tedious, plodding tragedies rather than epic heroes’ journeys.

It’s tempting to self-mythologise and condense this history – sorry, narrative – into a kind of highlights package. But that would skip most of the interesting lessons. Trade Me, Xero, Vend and Timely are all success stories. What is less known, but just as remarkable, is how close they all came to being failures. Let’s start with the near-death experiences.

2001: Trade Me

Trade Me was only two years old and still fragile. Our small team had signed up more than 100,000 members. We were hosting over 1,000 auctions every day, selling everything from antiques to watches. We were adding features to the website as fast as we could imagine them. That was exhilarating. But the business model was not working, which left us hanging by a thread. Our plan to provide free online classifieds, supported by advertising, had failed to generate the revenue required to fuel further growth.

The small pool of money – just $100,000 – that had been invested to get the business started was all but spent. The founder, Sam Morgan, pitched the company at a distressed valuation to every local venture capital fund, as well as to a bunch of large corporates. They all said, “no, thanks” (some didn’t bother with the “thanks”). The dot-com stock market bubble had burst. Would-be investors were deeply sceptical about the potential of internet businesses. The company was being propped up by loans from existing shareholders.

I had only recently become a shareholder myself. I didn’t have any cash to lend, but I did work for several months at a significantly reduced salary. Eventually that became untenable. The lure of highly paid work overseas was too much. If I’m honest, when I packed my bags, I didn’t expect Trade Me would be there to come back to. I was 25 years old. After two intense years, I figured the startup phase of my career might well be over.

I wasn’t the only one. Three of us from the original team of four left in quick succession, including Sam and his sister Jessi, who was the first employee, ahead of me. At one point, all three of us were living and working as contractors in London, leaving the fourth, my old friend Nigel Stanford, running things more or less by himself back in New Zealand. That period of time tends to get skipped over when the Trade Me story is told. Probably because it doesn’t fit the narrative.

One of the last changes we made to the website before I left was to start charging sellers a small “success fee” on each completed sale. It was less a brainwave than a last resort. We’d run out of other options to make money. Within a couple of years Sam, Jessi and I all returned to executive roles in the business. By then, those success fees were the centrepiece of a lucrative business model. In 2006 Trade Me was sold to Fairfax for $750 million.2

That outcome wasn’t obvious in 2001.

2009: Xero

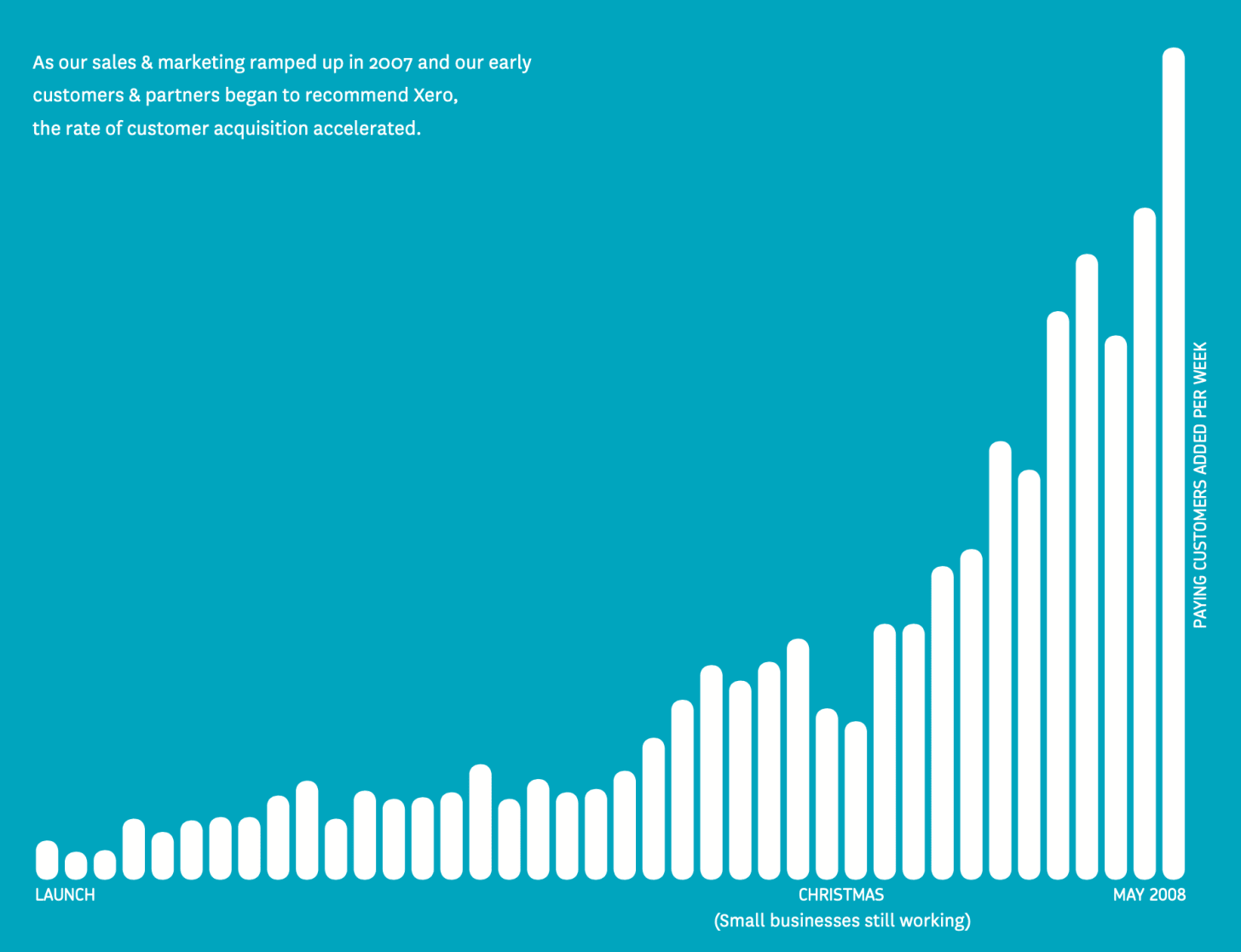

Some people, especially Australians, think that the Xero story starts at the end of 2012, when shares in the online accounting software company were first listed on the Australian Stock Exchange. The share price then was A$4.65. By early 2014 it had jumped nearly tenfold to over A$45. But there is a long pre-history prior to those glory days, where the share market wasn’t nearly as positive and the outcome for the company was much more uncertain.

I invested and joined the team in 2007, just prior to the float on the much smaller New Zealand Stock Exchange. That listing valued the company at NZ$55 million, and raised $15 million of new capital at $1 per share. For several years after that the share price languished below the listing price. In public, at least, co-founders Rod Drury and Hamish Edwards were full of bravado. But despite the stated global ambitions, there was pretty modest customer traction, almost entirely in New Zealand.

In the prospectus for the initial public offering – or IPO – we had cautiously forecast that the company would have 1,300 subscribers by the end of the first year while hoping for a whole lot more.3 The actual result we achieved was only 1,406, and about 40% of those new customers signed up in the final five weeks.

Millions had been invested, but the income from customer subscriptions was tiny – just $134,000 in the first year. We made more from the interest on investors’ dollars sitting in the bank account. It was an anxious time. The large, well-paid team was burning through that pile of cash. It wasn’t obvious that the stock market would be patient for long. One analyst speculated that we could be the first public company to be named after our share price.4 There was a high turnover of senior staff, especially in sales and marketing. I was one of those who left. Thankfully, I didn’t table-flip and sell my shares on the way out.

With its fate hanging in the balance, in 2009, Xero raised $23 million of new capital from MYOB founder Craig Winkler.5 MYOB was the incumbent accounting software provider that Xero was hoping to disrupt in both New Zealand and Australia. Craig had only quit as CEO a year prior to that after MYOB shareholders had bafflingly blocked his share option grant.6 Craig decided to back Xero instead. He purchased 24% of the company for 90c per share – 10% less than the price paid by investors who had backed the company in the IPO two years earlier. It turned out to be an inspired decision.

The sales team, by then led by Leanne Graham, shifted to focus on selling to accountants rather than directly to small businesses. That was a turning point. Within three years Xero would raise a further $170 million of capital. The number of subscribers increased from 6,000 to 78,000. Revenue increased 20-fold. Today it has millions of subscribers around the world and is valued at more than A$20 billion.

That outcome wasn’t obvious in 2009.

2015: Vend

I was one of the original investors in Vend in 2010. To even call it a company back then was slightly misleading. It was really just a founder, the magnificently moustachioed Vaughan Rowsell, and his wife, Mel. They had an idea to build cloud-based point-of-sale software for small retailers. In the crazy five years that followed we raised more than $35 million of capital from international venture capital funds. We hired 250 people. We became a global business, with just 15% of our revenue coming from New Zealand. Our customers included ice-cream stores in Russia and garden supply stores in the Cook Islands. It felt like everything we touched turned to gold. We won both Emerging Company and Exporter of the Year at the Hi-Tech Awards.7 We ranked fourth on the 2014 Deloitte Fast 50 list of the most rapidly growing companies in the country. We were expanding at an eye-watering pace but were at the tail end of an era when “rank well on Google” was a sufficient marketing strategy. We were also burning serious amounts of cash. Too much. By the end of 2015 we came very close to shutting it all down.

Our plans for the future factored in a new investor who had agreed to fund the next stage of the business. When they changed their mind at the last minute it left us with hard decisions to make and no time left to make them. Because we were spending much more than we earned we were, to use the description coined by Y Combinator founder Paul Graham: “Default dead.”8 We had chosen a growth path that required us to get permission to continue to exist from investors every 12-18 months, and our time had suddenly run out. We had chosen a growth path that required us to go cap in hand to investors every 12 to 18 months. Our time had suddenly run out.

When all this was unfolding, I was in Berlin, with fellow director Barry Brott from Square Peg, an Australian venture fund and our largest investor, and Kimberley Gilmour, our head of people and culture. We had intended to meet our freshly recruited European sales and support team. Instead we spent the day informing them that we would need to close the office and they would all be out of a job.

I tried to track down Vaughan, but he was missing in action. So from our hotel in Prenzlauer Berg, in the former East Berlin, Barry and I stayed up into the night on a series of urgent phone calls with existing shareholders, hoping to confirm further funding. Not surprisingly, there was a range of reactions. Some of them offered very direct and not very complimentary or constructive feedback on my performance as chair of the board. Finding consensus was tricky. By the time we had reached everyone it was the early hours of the morning. We decided to head out for some food, and got flashed by a drunk German teenager in the hotel elevator. I was too exhausted to do anything other than vacantly laugh. I don’t think that was the reaction he was expecting.

A couple of days later I flew back to Auckland and checked into a budget hotel in Newmarket, just down the road from the recently refurbished and suddenly much too large Vend headquarters. A barrage of urgent decisions awaited us. We had to make a number of people redundant, including some who had worked in the business for a long time and done the hard yards. That was painful for everybody, especially those who lost their jobs through no fault of their own. Anybody who thinks it’s difficult to grow a successful startup should try rapidly shrinking one. It’s much harder.

Without those emergency measures it would have been all over. Even with them it wasn’t clear we’d survive. In the weeks that followed we forged on, found a more sustainable path and confirmed new funding, mostly from existing shareholders. Within a few months there was an overhaul of the exec team and board (Barry was the only survivor – what happened to me is a story for another time) but the business continued.

In 2021 Vend was acquired by Lightspeed, one of our fiercest competitors in those early days, for $485 million.9

That outcome wasn’t obvious in 2015.

2020: Timely

Timely was on the brink of becoming one of the first startups to fall victim to the Covid-19 pandemic. I’d been involved since 2013, when co-founders Ryan Baker and Andrew Schofield had convinced me to become the first investor in their fledgling online bookings software venture. They were not typical founders. They were quietly confident, considered and measured. More than any other founders I’ve worked with, they were always keen to listen and adjust based on the advice they got. We never got ahead of ourselves.

Our customers were hairdressers, beauty salons, and spas. As the virus started to spread around the world, in early 2020, the vast majority suddenly shut their doors. We watched forward bookings evaporate as the world went into isolation. It was obvious this was going to be a real test for all of us. Rather than hide from that fact, we shared the data publicly. I know many people in the health and beauty sector found that incredibly useful as they worked on their own response.

We took the same approach internally. The impact on our subscription revenue wasn’t pretty. We had no idea how much longer this would continue, but the forecast bank balance trended pretty quickly to zero. We shared metrics with the whole team showing the revenue impact and the amount of cash we needed to stay afloat. Giving everybody the information they needed to make good decisions was crucial.

We had to immediately bury our old plans. That required remarkable leadership. Ryan, who with his executives had spent the last few years building an impressive team, committed to preserving every job. We offered generous discounts to customers. We immediately cut board fees to zero and made deep cuts to executive salaries. Next we asked the rest of the team what they could do to help. As Ryan told everybody:10

All of us will be affected a little so that none of us has to be affected a lot.

We managed to reduce an already lean cost base by 20%. Some staff agreed to bigger cuts so that others, who would be more heavily impacted, didn’t have to. It was an amazing collective response, creating a positive feedback loop. With job security, the whole team focused on helping customers navigate the lockdowns, providing whatever support we could. We retained the bulk of our customer base, albeit on reduced subscriptions. As competitors dealt with their own survival we even gained market share. That additional revenue allowed us to keep the cycle going.

Remarkably, within a few months we were able to repay staff the salaries that had been cut. Soon we began the conversations that would lead to the sale to US software company EverCommerce. One of the terms of that acquisition was that the Covid wage subsidy we’d received from the New Zealand government was repaid, which was a satisfying full stop to this phase.11

That outcome wasn’t obvious in 2020, either.

Hold on tight

Sudden plunges like these cause whiplash for founders. A startup condenses intense experiences and changes people. These moments are stressful. They test, and sometimes break, working relationships. I’ve learned that the hard way.

These are moments of truth for investors and advisors too. It’s easy to support a successful company. When things go badly it separates people who are willing to roll up their sleeves and help from those who are just along for the ride. Typically these are expensive lessons for those investors who continue to believe and are prepared to step up in the short term. They’re also the most rewarding, in both senses of that word, when it works out.

It’s easy to dismiss Trade Me, Xero, Vend and Timely as outliers. But that misses the most important thing I learned from working on all of them: none was obviously successful in the beginning, and all of them felt like imminent failures at many stages in the middle. I have mental scar tissue from each of those stories. They taught me how to be wrong. Amazingly, all had happy endings.

It doesn’t always work out this way.

-

This was really highlighted to me when I watched The Social Network movie about the early stages of Facebook. In one scene they are a small team struggling away in a house in Palo Alto, and nobody has heard of them. Then, it jumps quickly to them moving into their first office and celebrating 1 million users. As if that just happened while they weren’t looking! I couldn’t help but feel like they just skipped over all of the most interesting bits in the story, in a montage. ↩︎

-

Trade Me sold for $700m, NZ Herald, 8th March 2006. ↩︎

-

The 2007 prospectus also contained this wildly optimistic estimate of the breakeven point: “New Zealand revenue will begin to exceed its New Zealand cost base at around 8,000 customers.” And on profitability: “Directors do not currently expect that Xero will record an overall profit for at least three years.” It actually took 13 years. ↩︎

-

Xero (XRO.NZ) – Thoughts on Valuation, Clare Capital, 3rd October, 2013. ↩︎

-

MYOB founder buys into rival, Sydney Morning Herald, 7th April, 2009. ↩︎

-

MYOB shareholders vote down options allocation, Sydney Morning Herald, 25th April, 2008. ↩︎

-

Vend raises $25 million, celebrates at NZ Hi-Tech Awards event, iStart, 27th March 2014. ↩︎

-

Default Alive or Default Dead?, by Paul Graham. ↩︎

-

Lightspeed to acquire Vend to power global retail expansion, Lightspeed, 11th March 2021. ↩︎

-

Ryan Baker, Twitter, July 2020. ↩︎

-

EverCommerce Completes Acquisition of Timely, Leading Business Management Software for Beauty Industries, EverCommerce, 8th July 2021. ↩︎